Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Is your house sitting and not selling? It may be time to reconsider your asking price. Want some expert advice on what you should do? Talk to your agent. Don’t have an agent? Reach out! I am never too busy to make a connection.

Data Sources:

Is your house sitting and not selling? It may be time to reconsider your asking price. Want some expert advice on what you should do? Talk to your agent. Don’t have an agent? Reach out! I am never too busy to make a connection.

Data Sources:

You’ve got big plans for 2026. But what you do this year could be the difference between a smooth sale and a stressful one. If you’re thinking of selling next spring (the busiest season in real estate), the smartest move you can make is to start prepping now. As Realtor.com says:

“If you’re aiming to sell in 2026, now is the time to start preparing, especially if you want to maximize the spring market’s higher buyer activity.”

Because the reality is, from small repairs to touch-ups and decluttering, the earlier you start, the easier it’ll be when you’re ready to list. And, the better your house will look when it’s time for it to hit the market.

Talk to any good agent and they’ll tell you that you can’t afford to skip repairs in today’s market. There are more homes for sale right now than there have been in years. And since buyers have more to choose from, your house is going to need to look its best to stand out and get the attention it deserves.

Now, that doesn’t mean you have to do a full-on renovation. But it does mean you’ll want to tackle some projects before you sell. Your house will sell if it’s prepped right. And you don’t want to be left scrambling in the spring to get the work done.

Because here’s the advantage you have now. If you start this year, you’ll be able to space those upgrades and fixes out however you want to. More time. Less stress. No sense of being rushed or racing the clock.

Whether it’s fixing that leaky faucet, repainting your front door, or finally replacing your roof, you can do it right if you start now. And you have the time to find great contractors without blowing your budget or paying extra for rushed jobs.

To figure out what’s worth doing and what’s not in your market, you need to talk to a local agent early. That way you’re not wasting your time or money on something that won’t help your bottom line. As Realtor.com explains:

“Respondents overwhelmingly agree that both buyers and sellers enjoy a smoother, more successful experience when they start early. In fact, a recent survey reveals that, for sellers, bringing a real estate agent into the process sooner can pay off significantly.”

A skilled agent can tell you:

And having that information up front is a game changer.

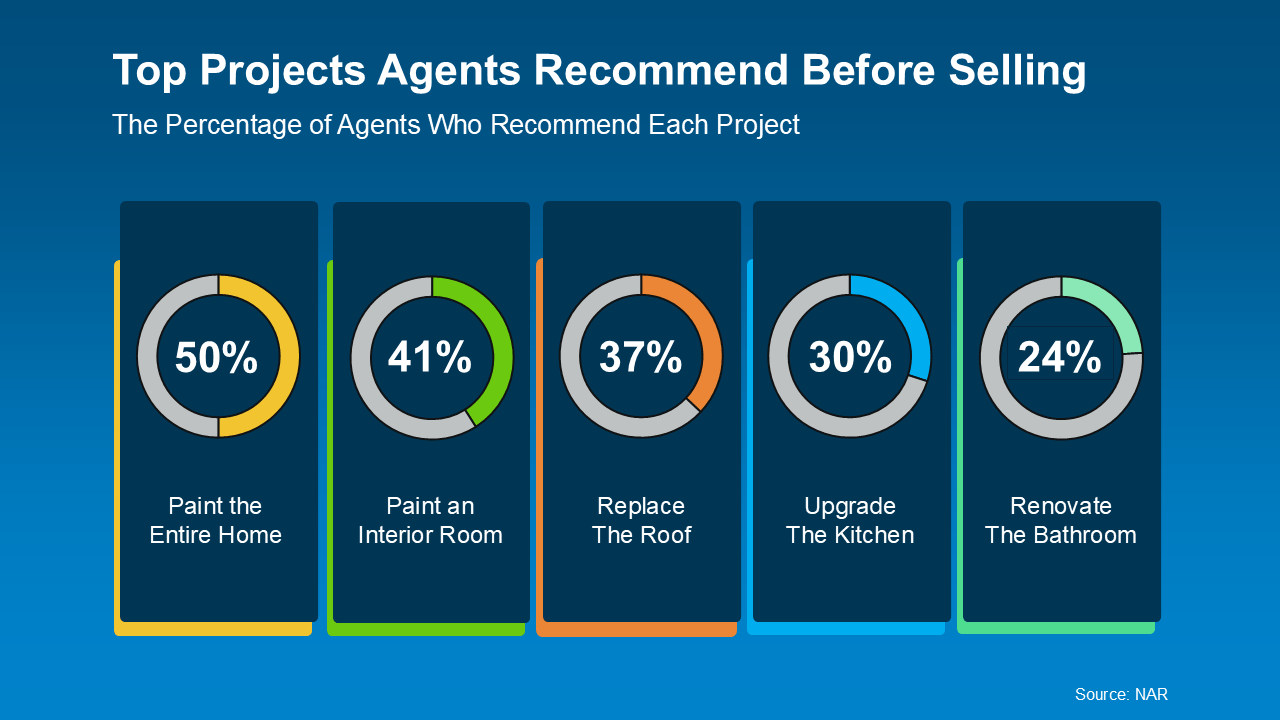

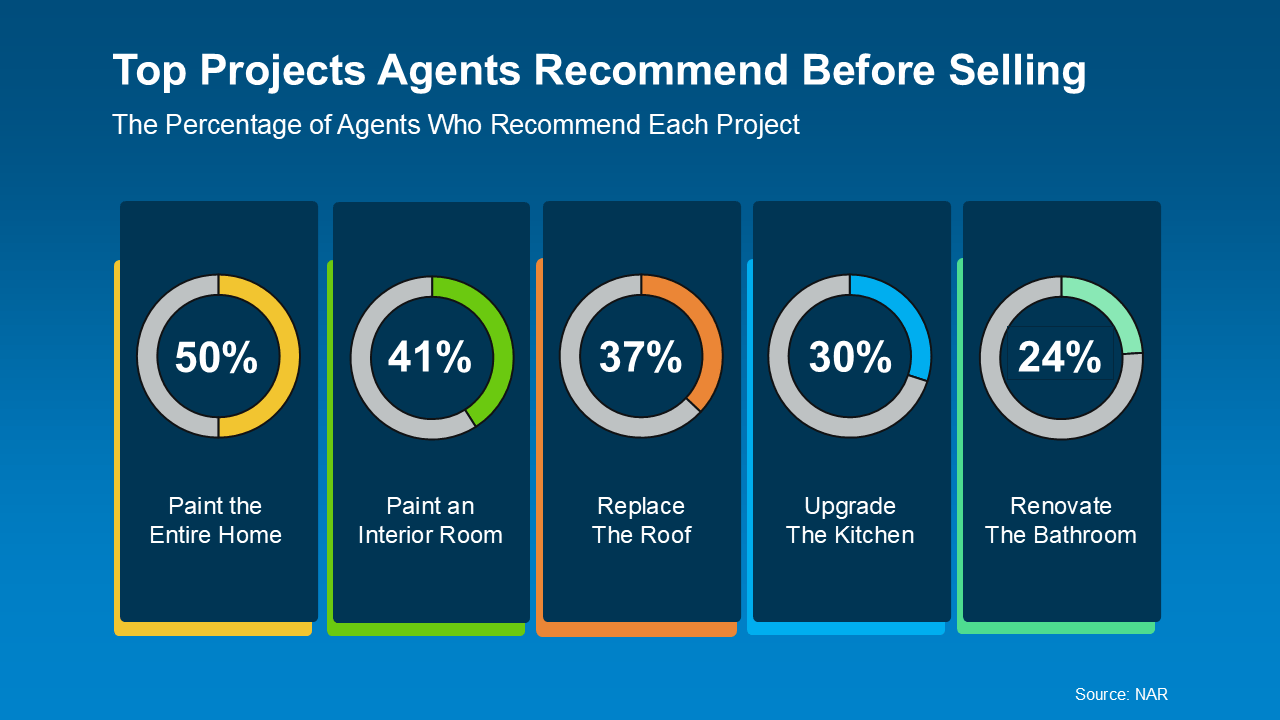

To give you a rough idea of what may come up in that conversation, here are the most common updates agents are recommending today, according to research from the National Association of Realtors (NAR):

Just remember, what’s worth updating really depends on the homes you’re competing with in your market. Some areas don’t have a ton of inventory, so little updates may be all you need to tackle. In other areas, there are far more homes for sale, so you may need to do a bit more to make your house stand out.

Just remember, what’s worth updating really depends on the homes you’re competing with in your market. Some areas don’t have a ton of inventory, so little updates may be all you need to tackle. In other areas, there are far more homes for sale, so you may need to do a bit more to make your house stand out.

Your agent will walk you through what you need to do for your specific house and market. And that’s expertise that’ll really pay off.

If your plan is to sell in 2026, it’s time to get serious. Taking some time to prep means you’ll hit the market confident, ready, and ahead of other sellers who waited until January to get started.

Want to know which projects are getting the biggest return on their investment in our market? Let’s connect so you can head into next spring with a solid game plan.

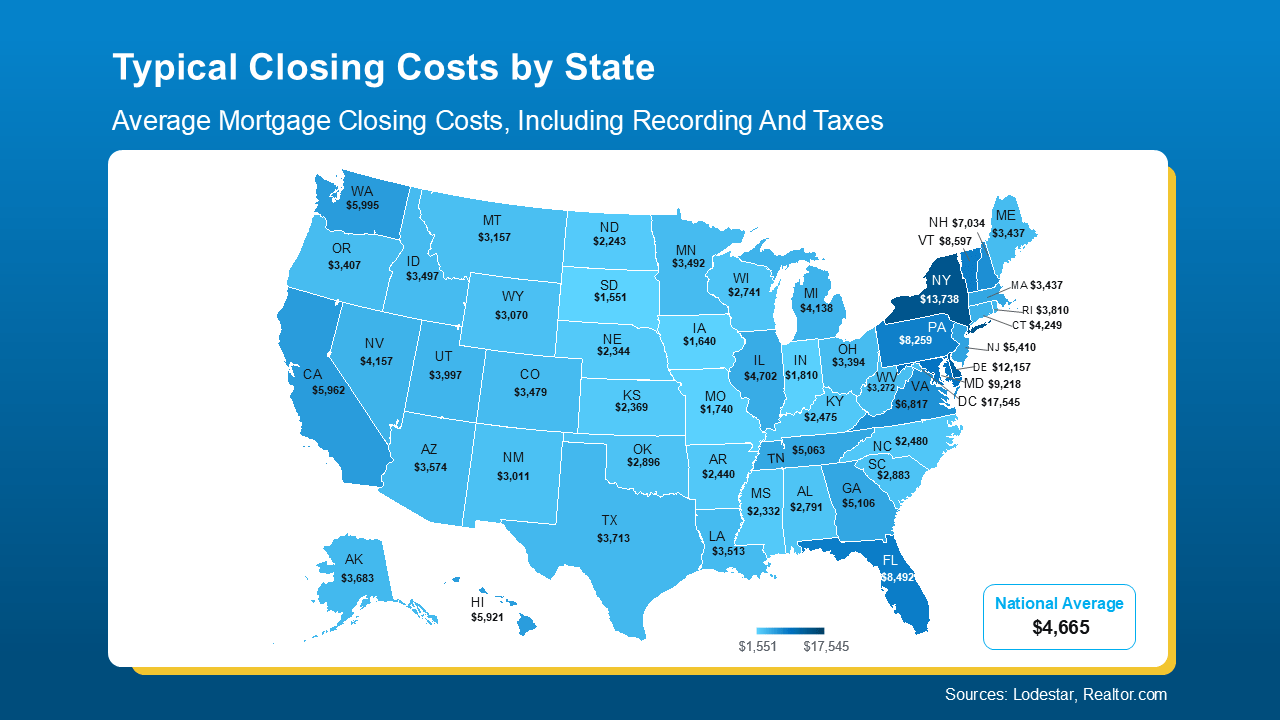

If you’re planning to buy a home this year, there’s one expense you can’t afford to overlook: closing costs.

Almost every buyer knows they exist, but not that many know exactly what they cover, or how different they can be based on where you’re buying. So, let’s break them down.

Your closing costs are the additional fees and payments you make when finalizing your home purchase. Every buyer has them. According to Freddie Mac, they typically include things like homeowner insurance and title insurance, as well as various fees for your:

When you search for information about closing costs online, you’ll often see a national range, usually 2% to 5% of the home’s purchase price. While that’s a useful starting point if you’re working on your homebuying budget, it doesn’t tell the whole story. In reality, your closing costs will also vary based on:

While the home price is obviously going to matter, state laws, tax rates, and even the going costs for title and attorney services can change what you expect to pay. That’s why it’s important to talk to the pros ahead of time so you know what to budget for. It can put you in control before you even start shopping.

To give you a rough ballpark, here’s a state-by-state look at typical closing costs right now based on those factors for the median-priced home in each state (see map below):

As the map shows, in some states, typical closing costs are just roughly $1-3K. In a few places, they can be closer to $10-15K. That’s a big swing, especially if you’re buying your first home. And that’s why knowing what to expect matters.

As the map shows, in some states, typical closing costs are just roughly $1-3K. In a few places, they can be closer to $10-15K. That’s a big swing, especially if you’re buying your first home. And that’s why knowing what to expect matters.

If you want a real number to help with your budget, your best bet is to talk to a local agent and a lender. They can run the math for your price range, loan type, and exact location.

And just in case you’re looking at your state’s number and wondering if there’s any way to trim that bill, NerdWallet shares a few strategies that can help:

Closing costs are a key part of buying a home, but they can vary more than most people realize. Knowing your numbers (and how to potentially bring them down) can go a long way and help you feel confident about your purchase.

Let’s look at typical closing costs in our area and get you a personalized estimate, so you can craft your ideal budget.

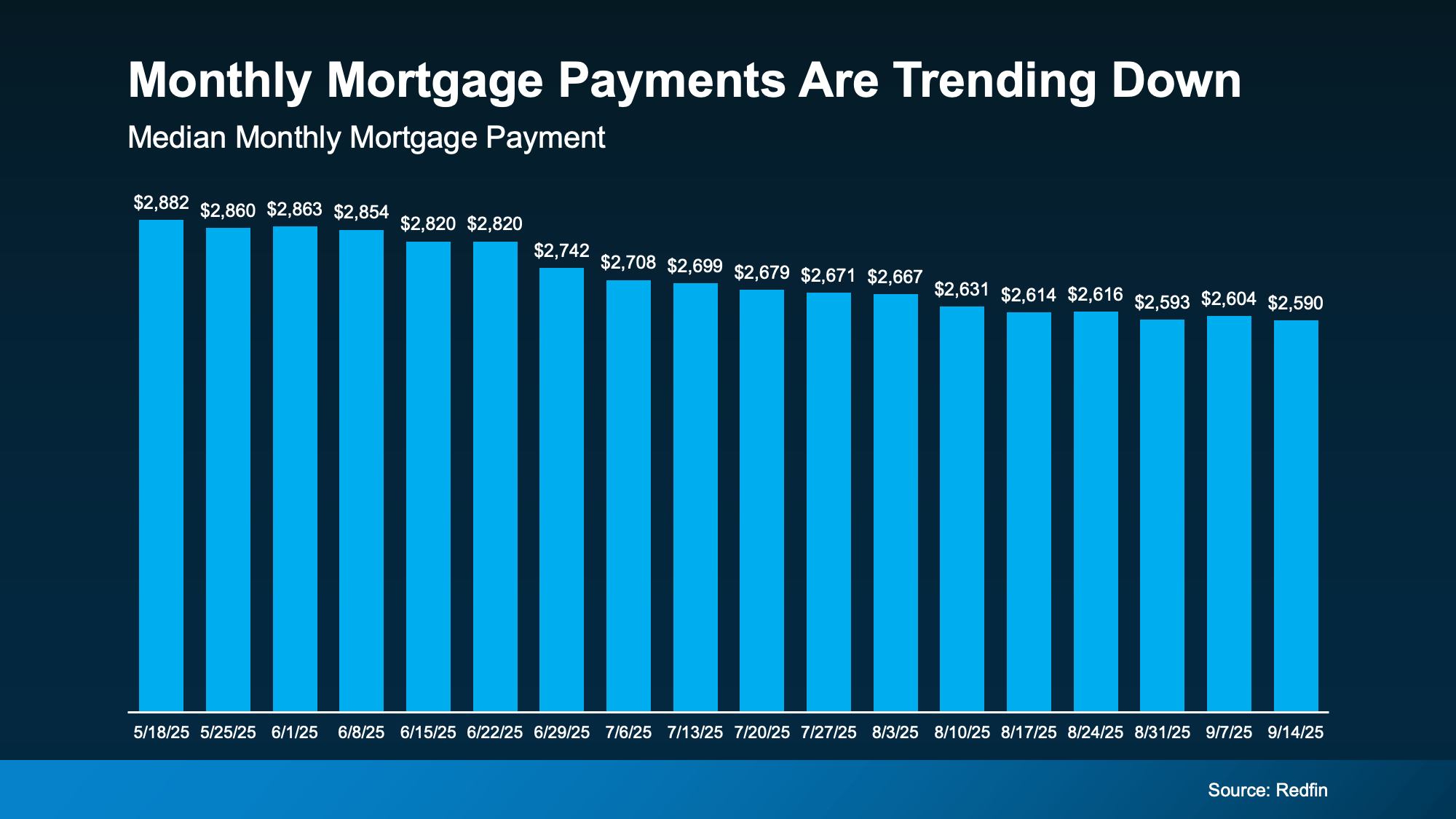

For the past couple of years, it’s been tough for a lot of homebuyers to make the numbers work. Home prices shot up. Mortgage rates too. And a number of people hit pause because it just didn’t feel possible. Maybe you were one of them.

But there’s some encouraging news. If you’ve been waiting for a better time to jump back in, affordability may finally be showing signs of improvement this fall.

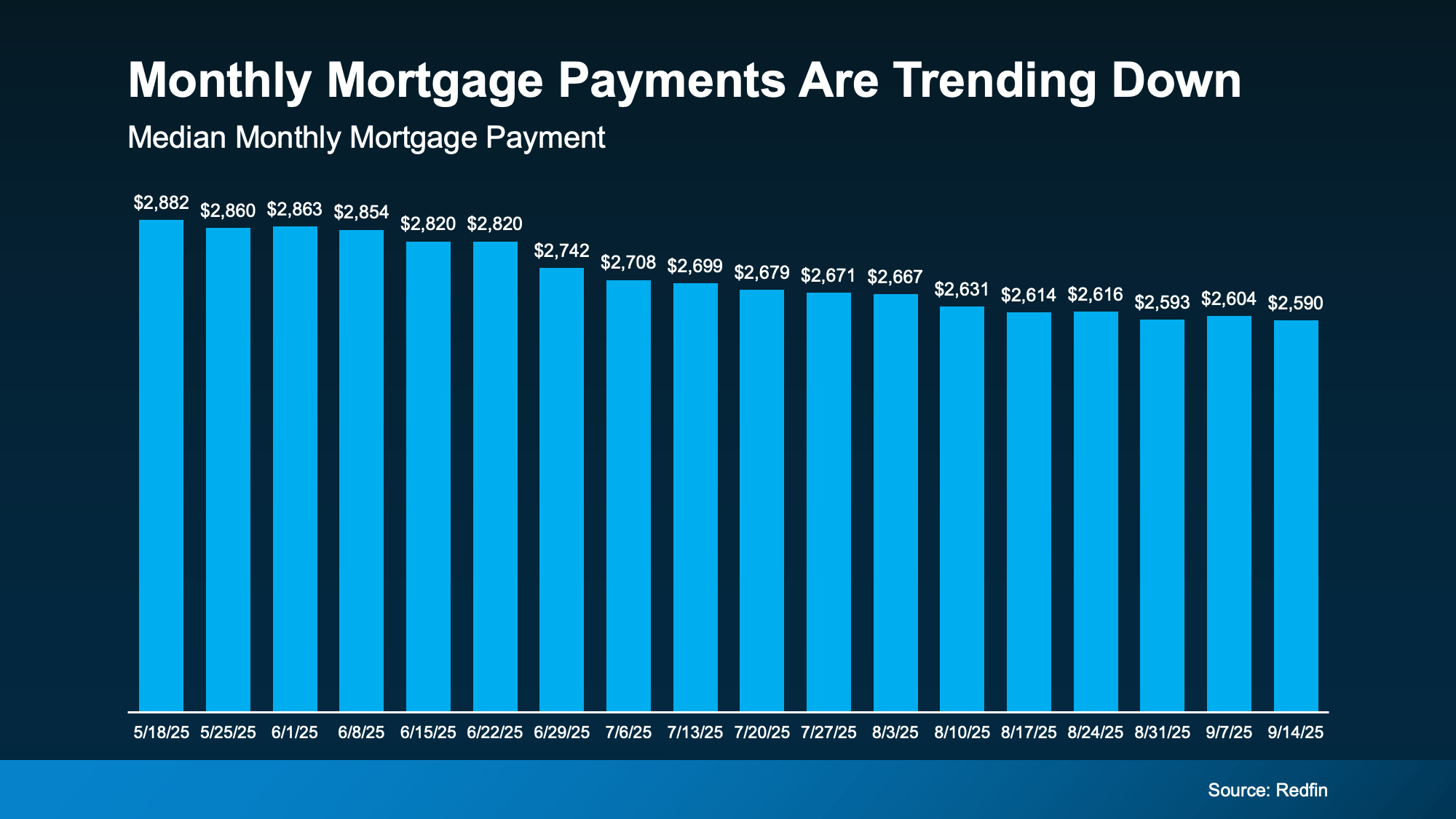

The latest data from Redfin shows the typical monthly mortgage payment has been coming down, and is now about $290 lower than it was just a few months ago (see graph below):

And here’s why this is happening. The cost of buying a home really comes down to three things:

And here’s why this is happening. The cost of buying a home really comes down to three things:

Right now, all three are finally moving in a better direction for you. While that doesn’t mean it’s suddenly easy to buy at today’s rates and prices, it does mean it’s not as challenging.

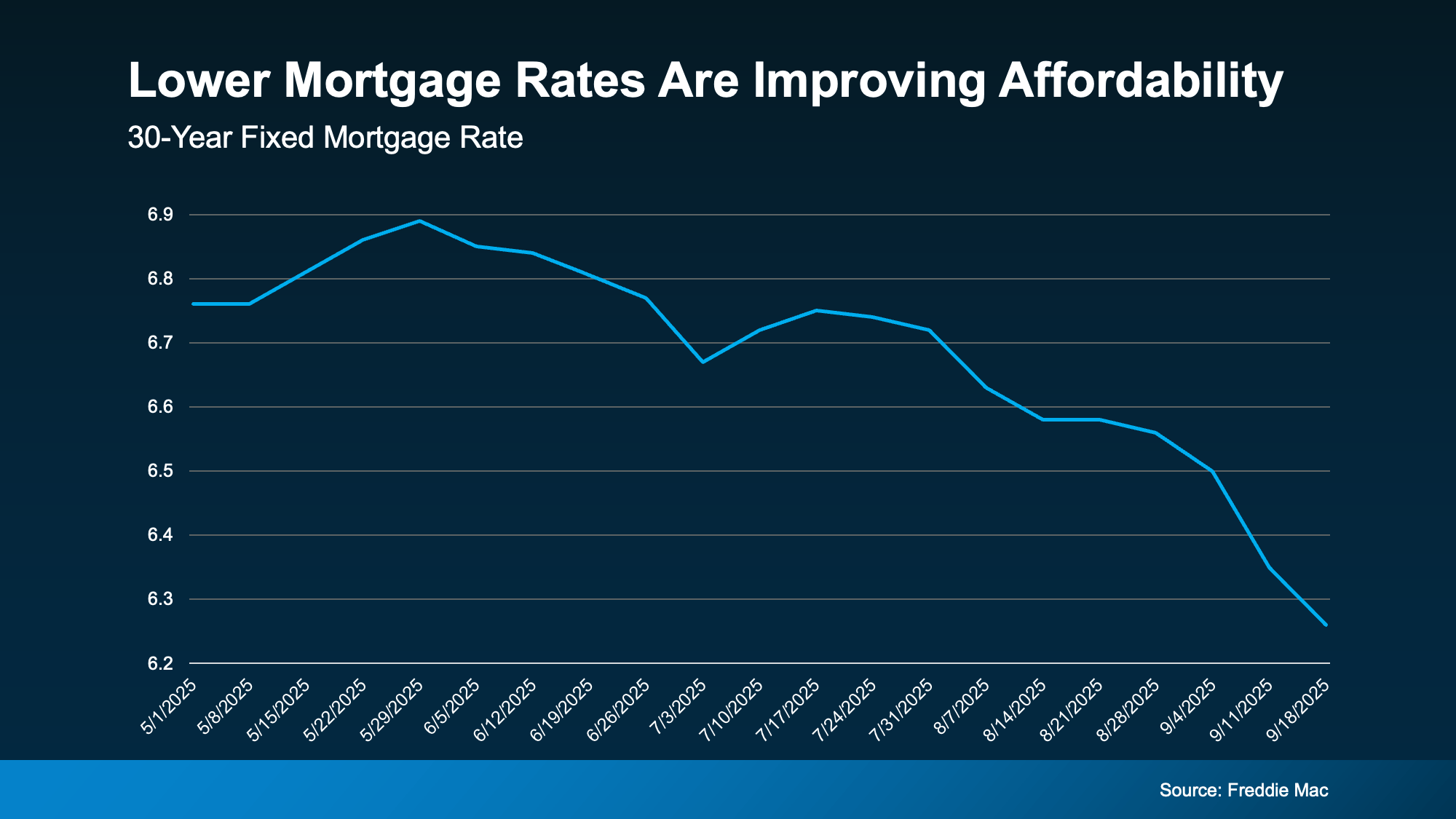

Mortgage rates have come down compared to earlier this year. In May, they were roughly 7%. And now, they’re closer to 6.3% (see graph below):

That may not sound like a big deal, but it does matter. Even small changes in rates can make a difference in your future monthly payment. Compared to when rates were 7%, if you take out an average $400K mortgage now at 6.3%, it’ll cost about $190 less a month based on just rates alone.

That may not sound like a big deal, but it does matter. Even small changes in rates can make a difference in your future monthly payment. Compared to when rates were 7%, if you take out an average $400K mortgage now at 6.3%, it’ll cost about $190 less a month based on just rates alone.

And for some people, that’s been enough to make buying a home possible again. As Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), explained on September 10th:

“The downward rate movement spurred the strongest week of borrower demand since 2022 . . . Purchase applications increased to the highest level since July and continued to run more than 20 percent ahead of last year’s pace.”

After several years of prices rising very rapidly, price growth has finally slowed. As Odeta Kushi, Deputy Chief Economist at First American, puts it:

“National home price growth remains positive, but muted — low single digits — and we expect this trend to continue in the second half of the year.”

For buyers, that’s actually a big relief. That moderation makes it easier to plan your budget. And in some markets, prices have even dipped slightly. If you’re in one of the markets, you may be able to find something that’s more affordable than you’d expect.

According to the Bureau of Labor Statistics (BLS), wages are up near 4% annually. Lawrence Yun, Chief Economist at NAR, explains why that number is so important right now:

“Wage growth is now comfortably outpacing home price growth, and buyers have more choices.”

In other words, the typical paycheck is rising faster than home prices right now, which helps make buying a little more affordable. Now, it’s not a big difference, but in a market like this, every bit counts.

Lower rates, slower price growth, and stronger wages might be enough to make the numbers finally work for you this fall.

While affordability is still tight, it’s a little easier on your wallet to buy now than it was just few months ago. Remember, data from Redfin shows the typical monthly mortgage payment is already around $290 lower than it was earlier this year.

Have you been wondering if it’s worth taking another look at buying?

Let’s run the numbers together. We can go over your budget, see what’s changed, and figure out if this fall is the time to turn window-shopping into key-turning.

You’ve been waiting for what feels like forever for mortgage rates to finally budge. And two weeks ago, they did – in a big way.

On Friday, September 5th, the average 30-year fixed mortgage rate fell to the lowest level since October 2024. It was the biggest one-day decline in over a year.

According to Mortgage News Daily, this was a reaction to the August jobs report, which came out weaker-than-expected for a second month in a row. That sent signals across the financial markets, and then mortgage rates came down as a result.

Basically, we’re seeing signs the economy may be slowing down, and as certainty grows in the direction the economy is going, the markets are reacting to what is likely ahead. That historically brings mortgage rates down.

But this isn’t just about one day of headlines or one report. It’s about what the drop means for you.

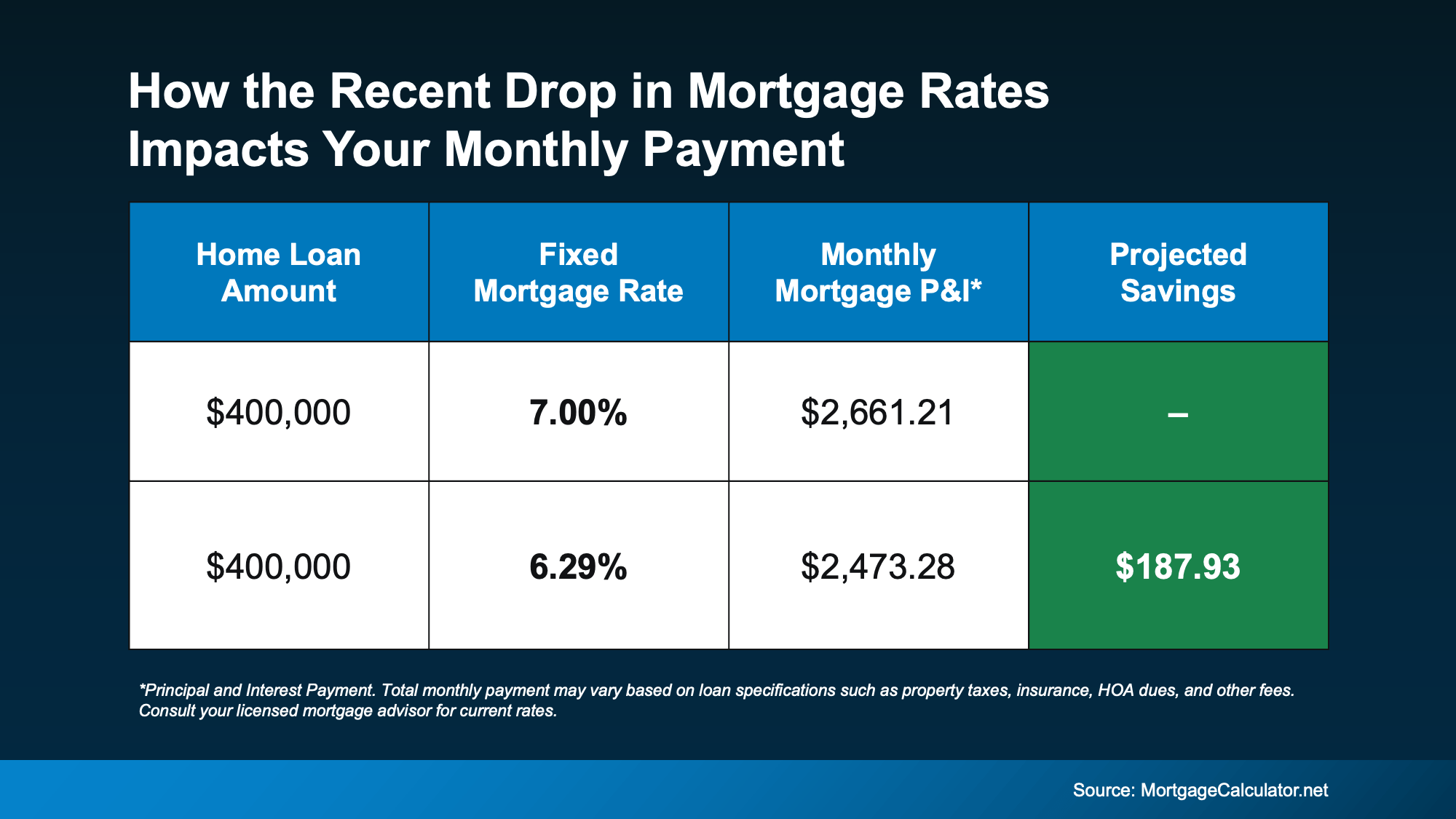

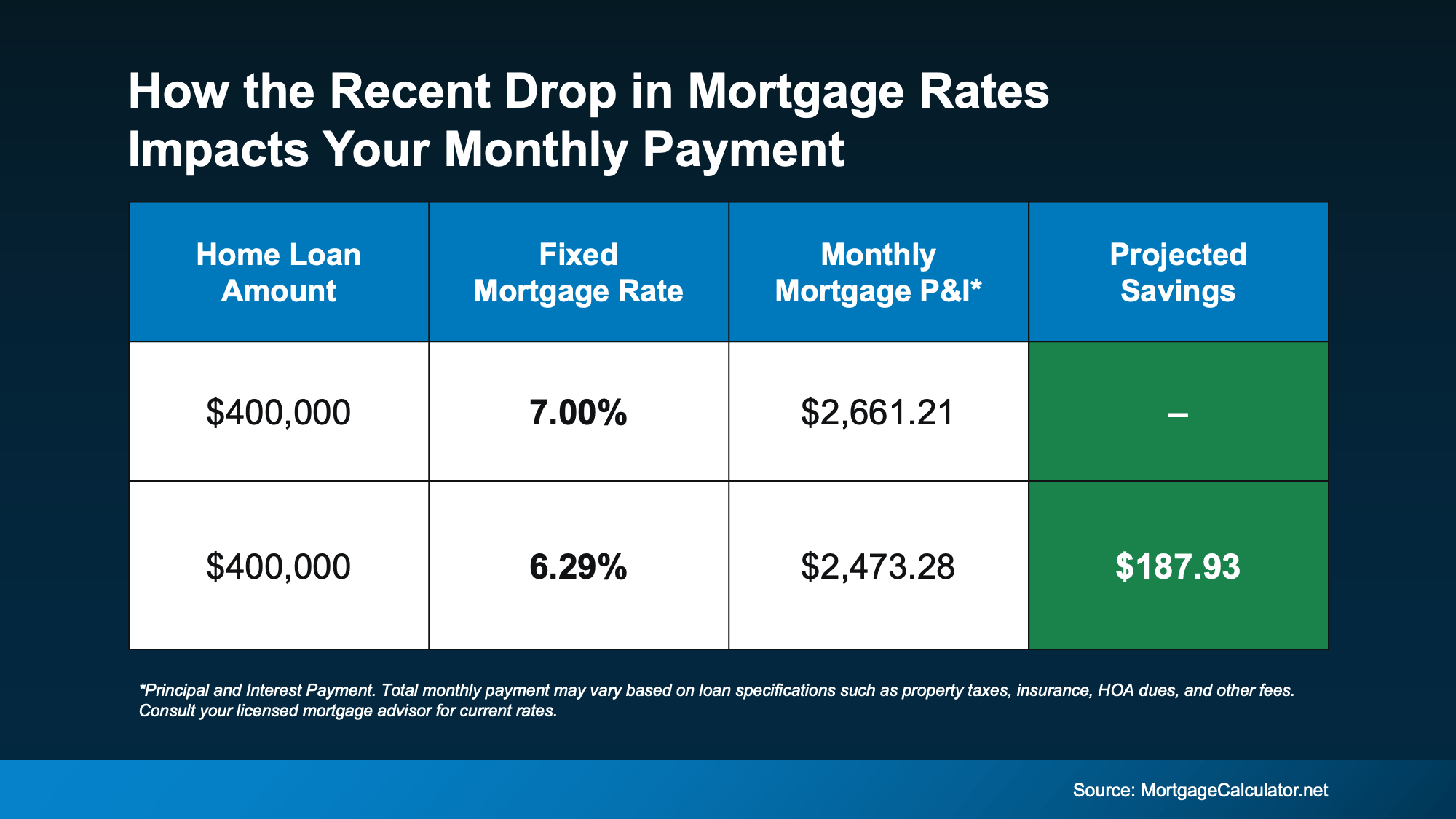

This recent change saves you money when you buy a home. The chart below shows you an example of what a monthly mortgage payment (principal and interest) would be at 7% (where mortgage rates were in May) versus where rates roughly are now:

Compared to just 4 months ago, your future monthly payment would be almost $200 less per month. That’s close to $2,400 a year in savings.

Compared to just 4 months ago, your future monthly payment would be almost $200 less per month. That’s close to $2,400 a year in savings.

That really depends on where the economy and inflation go from here. Rates could drop lower, or they could inch up slightly.

So, make sure you’re connected with a good agent and trusted lender. They’ll keep a close eye on inflation indicators, job market updates, and reactions to upcoming Fed policy to gauge where mortgage rates may go from here.

But for now, focus on this. While no one can say for sure where rates are headed, the fact that rates broke out of their months-long rut is a good thing. If you’ve been feeling stuck, this could make the start of a new chapter. As Diana Olick, Senior Real Estate and Climate Correspondent at CNBC, says:

“Rates are finally breaking out of the high 6% range, where they’ve been stuck for months.”

And that’s gives you more reason to hope than you’ve had in quite some time.

This is the shift you’ve been waiting for.

Mortgage rates just saw their biggest decline in over a year. And if rates stay near this level, it could make a home you couldn’t afford just a few months ago feel possible again.

What would today’s rates save you on your future monthly payment? Let’s connect so you can find out.

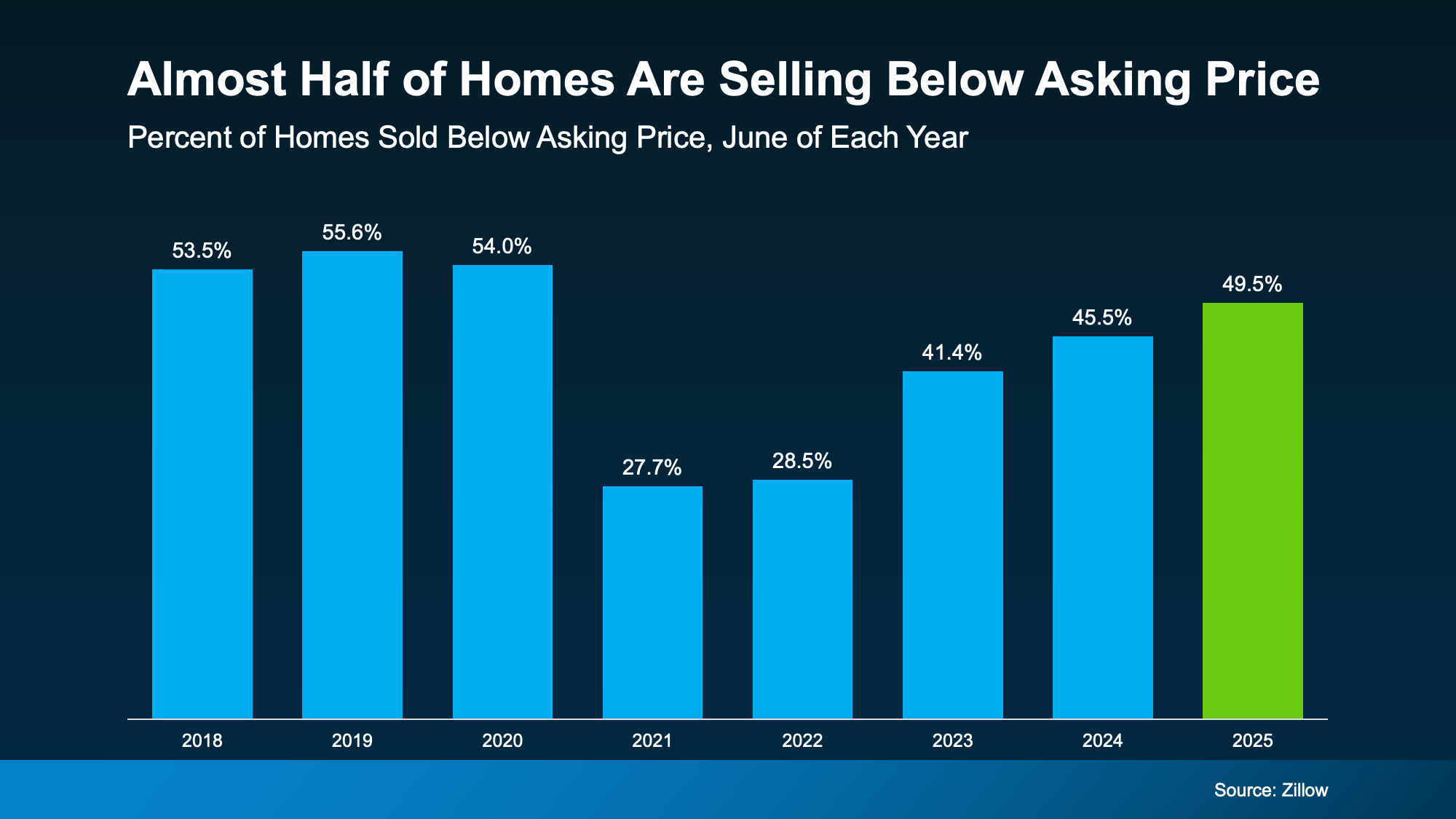

If your selling strategy still assumes you’ll get multiple offers over asking, it’s officially time for a reset. That frenzied seller’s market is behind us. And here are the numbers to prove it.

Right now, about 50% of homes on the market are selling for less than their asking price, according to the latest data from Cotality.

But that isn’t necessarily bad news, even if it feels like it. Here’s why. The wild run-up over the last few years was never going to be sustainable. The housing market needed a reset, and data shows that’s exactly what’s happening right now.

The graph below uses data from Zillow to show how this trend has shifted over time. Here’s what it tells us:

Why This Matters If You’re Selling Your House

Why This Matters If You’re Selling Your HouseIn this return to normal, your pricing strategy is more important than ever.

A few years ago, you could overprice your house and still get swarmed with offers. But now, buyers have more options, tighter budgets, and less urgency.

Today, your asking price can be make or break for your sale, especially right out of the gate. Your first two weeks on the market are the most important window because that’s when the most serious buyers are paying attention to your listing. Miss your price during that crucial period, and your sale will grind to a halt. Buyers will look right past it. And once your listing sits long enough to go stale, it’ll be hard to sell for your asking price.

Basically, sellers who cling to outdated expectations end up dealing with price cuts, lower offers, and a longer time just sitting on the market. But homeowners who understand what’s happening are still winning, even today.

Because that stat about 50% of homes selling for under asking also means the other half are selling at or above – as long as they’re priced right from the start.

So, how do you set yourself up for success? Do these 3 things:

If you want your house to be one that sells for at (or even more than) your asking price, it’s time to plan for the market you’re in today – not the one we saw a few years ago. And that’s exactly why you need a stand-out local agent.

You don’t want to fall behind in this market.

So, let’s talk about what buyers in our area are paying right now. With local expertise and a strategy that gets your house noticed in those crucial first two weeks, anything is possible.

Want to know what your house would sell for?

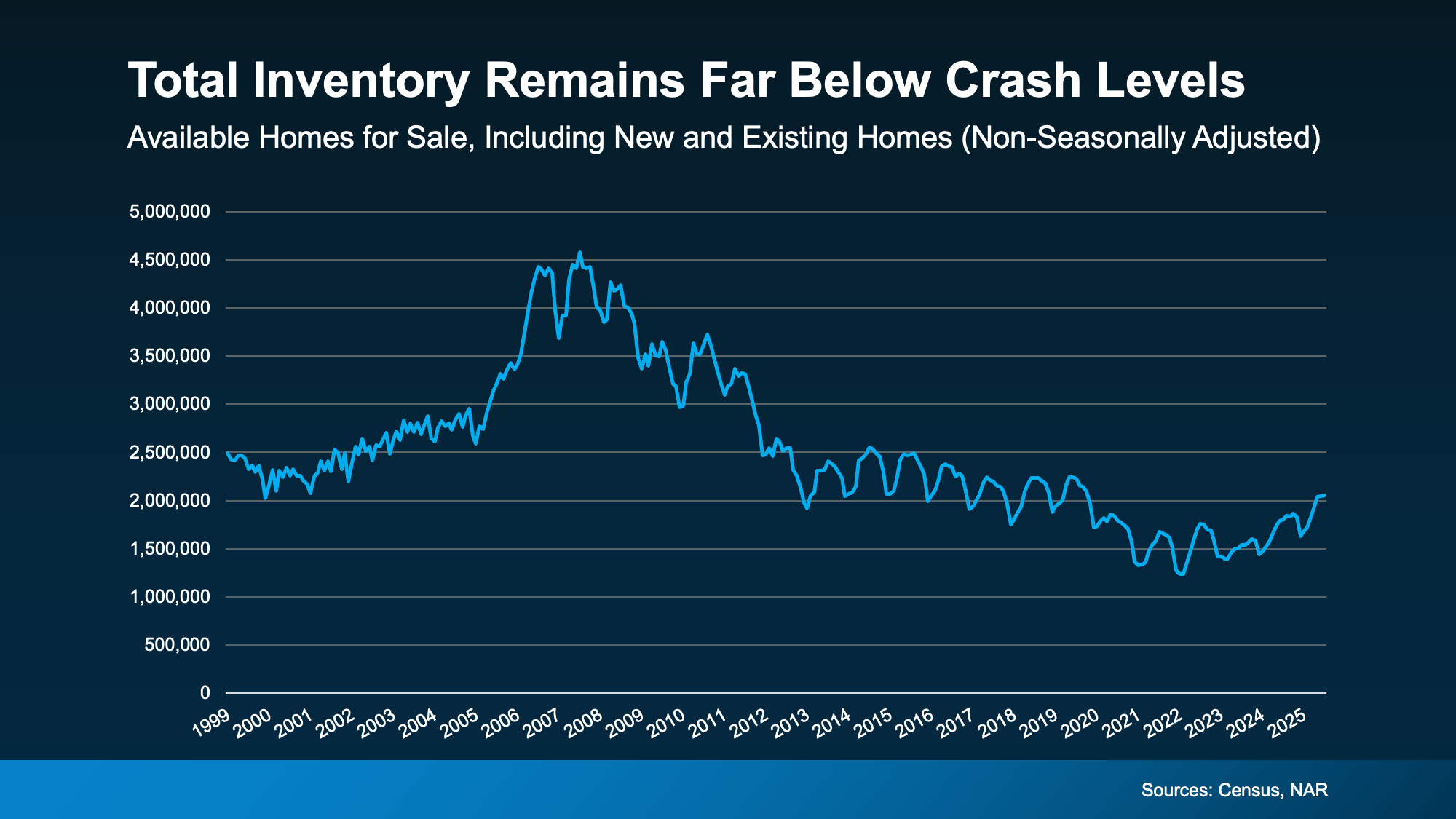

You may have seen talk online that new home inventory is at its highest level since the crash. And if you lived through the crash back in 2008, seeing new construction is up again may feel a little scary.

But here’s what you need to remember: a lot of what you see online is designed to get clicks. So, you may not be getting the full story. A closer look at the data and a little expert insight can change your perspective completely.

While it’s true the number of new homes on the market hit its highest level since the crash, that’s not a reason to worry. That’s because new builds are just one piece of the puzzle. They don’t tell the full story of what’s happening today.

To get the real picture of how much inventory we have and how it compares to the surplus we saw back then, you’ve got to look at both new homes and existing homes (homes that were lived in by a previous owner).

When you combine those two numbers, it’s clear overall supply looks very different today than it did around the crash (see graph below):

So, saying we’re near 2008 levels for new construction isn’t the same as the inventory surplus we did the last time.

So, saying we’re near 2008 levels for new construction isn’t the same as the inventory surplus we did the last time.

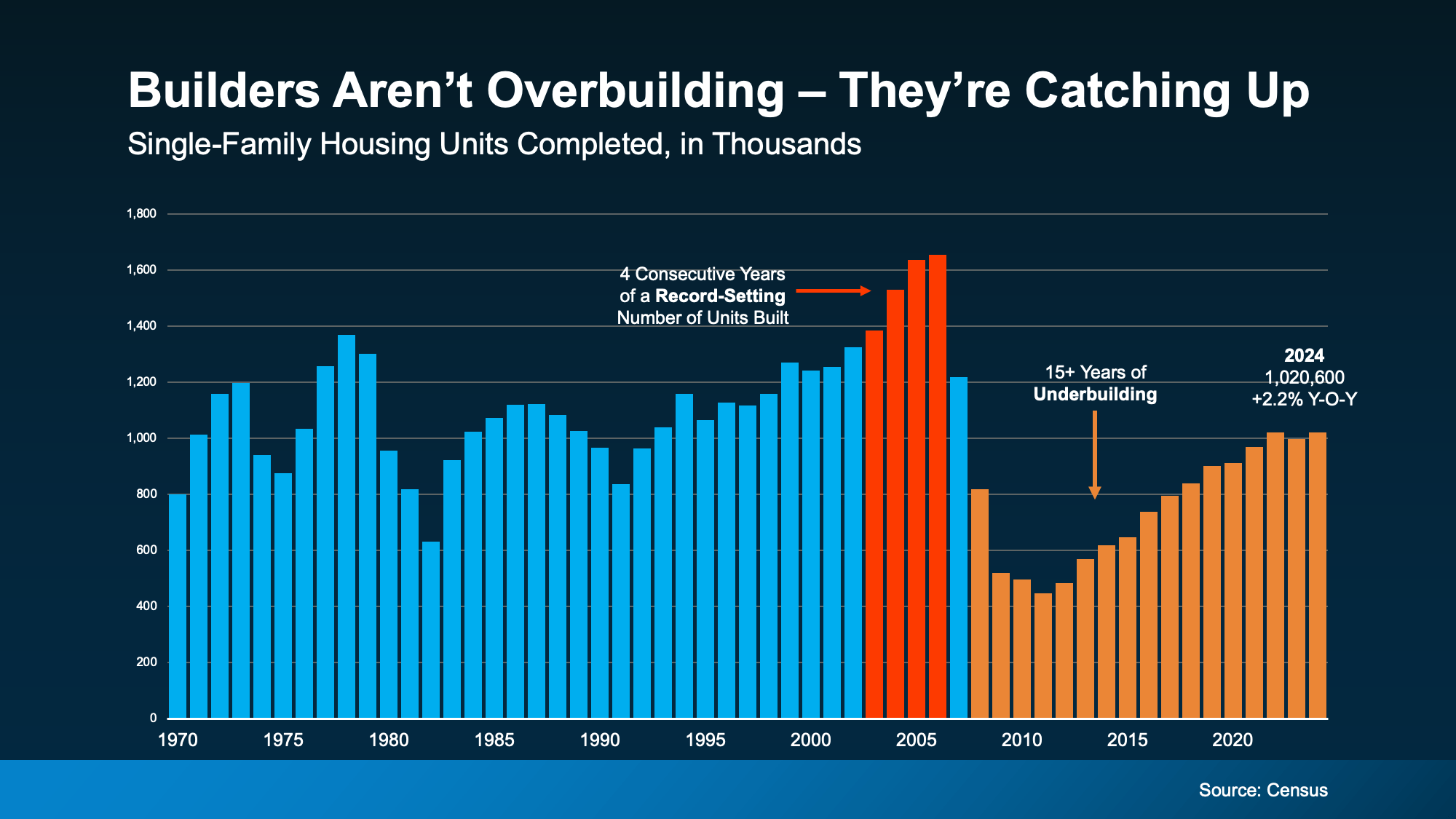

And here’s some other important perspective you’re not going to get from those headlines. After the 2008 crash, builders slammed on the brakes. For 15 years, they didn’t build enough homes to keep up with demand. That long stretch of underbuilding created a major housing shortage, which we’re still dealing with today.

The graph below uses Census data to show the overbuilding leading up to the crash (in red), and the period of underbuilding that followed (in orange):

Basically, we had more than 15 straight years of underbuilding – and we’re only recently starting to slowly climb out of that hole. But there’s still a long way to go (even with the growth we’ve seen lately). Experts at Realtor.com say it would roughly 7.5 years to build enough homes to close the gap.

Basically, we had more than 15 straight years of underbuilding – and we’re only recently starting to slowly climb out of that hole. But there’s still a long way to go (even with the growth we’ve seen lately). Experts at Realtor.com say it would roughly 7.5 years to build enough homes to close the gap.

Of course, like anything else in real estate, the level of supply and demand is going to vary by market. Some markets may have more homes for sale, some less. But nationally, this isn’t like the last time.

Just because there are more new homes for sale right now, it doesn’t mean we’re headed for a crash. The data shows today’s overall inventory situation is different.

If you have questions or want to talk about what builders are doing in our area, let’s connect.

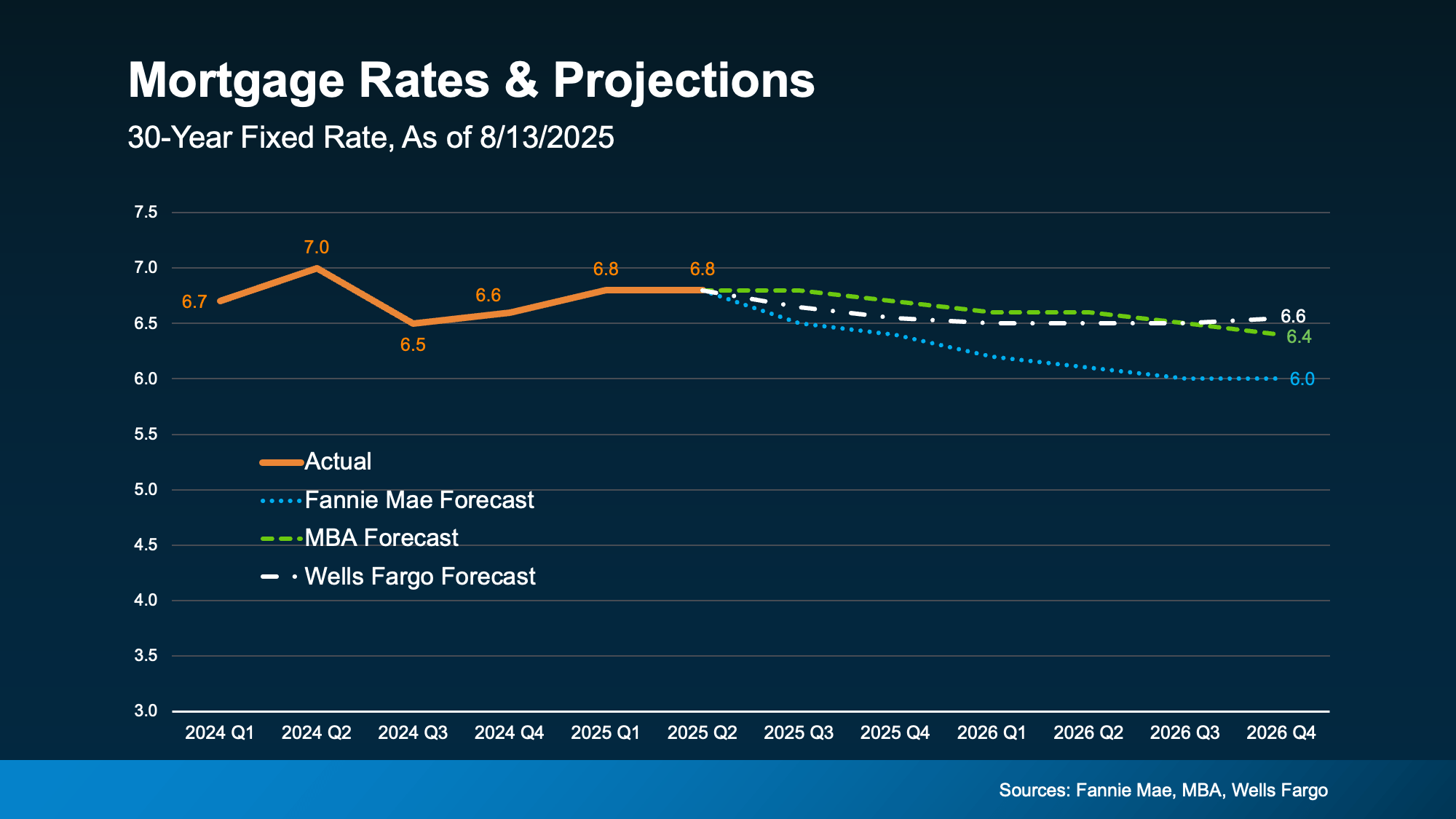

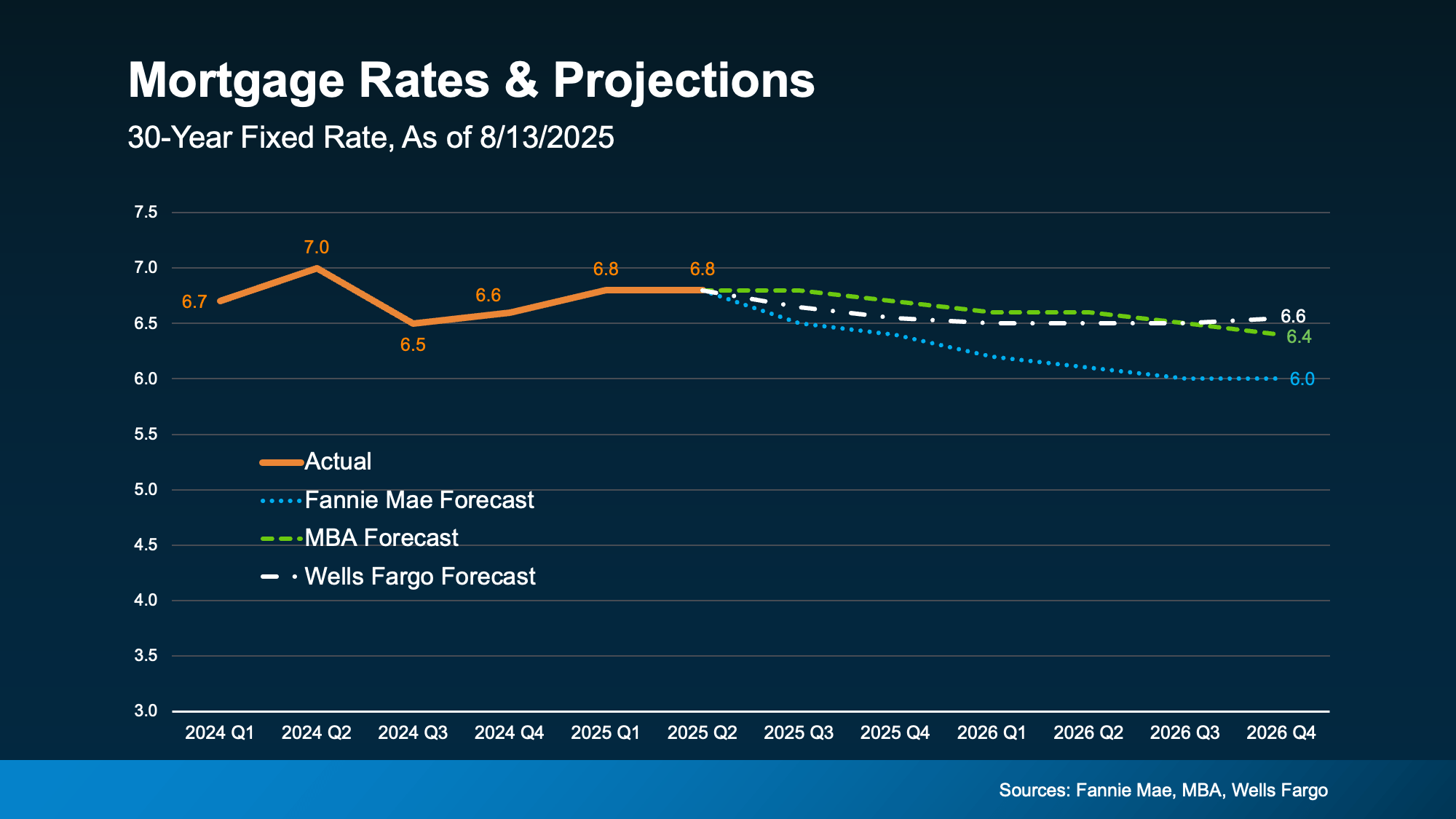

Mortgage rates are still a hot topic – and for good reason. After the most recent jobs report came out weaker than expected, the bond market reacted almost instantly. And, as a result, in early August mortgage rates dropped to their lowest point so far this year (6.55%).

While that may not sound like a big deal, pretty much every buyer has been waiting for rates to fall. And even a seemingly small drop like this reignites the hope we’re finally going to see rates trending down. But what’s realistic to expect?

According to the latest forecasts, rates aren’t expected to fall dramatically anytime soon. Most experts project they’ll stay somewhere in the mid-to-low 6% range through 2026 (see graph below):

In other words, no big changes are expected. But small shifts, like the one we just saw, are still likely.

In other words, no big changes are expected. But small shifts, like the one we just saw, are still likely.

Each time there’s changing economic news, there’s a chance mortgage rates will react. And with so many reports coming out this week, we’ll get a better feeling of where the economy and inflation are headed – and how rates will respond.

The magic number most buyers seem to be watching for is 6%. And it’s not just a psychological benchmark; it has real impact. A recent report from the National Association of Realtors (NAR) says if rates reach 6%:

That’s a lot of pent-up demand just waiting for the green light. And if you look back at the graph above, you’ll see Fannie Mae thinks we’ll hit that threshold next year. That raises an important question: Does it really make sense to wait for lower rates?

Because here’s the tradeoff. If you’re waiting for 6%, you need to realize a lot of other people are too. And when rates do continue to inch down and more buyers jump into the market all at once, you could face more competition, fewer choices, and higher home prices. NAR explains it like this:

“Home buyers wishing for lower mortgage interest rates may eventually get their wish, but for now, they’ll have to decide whether it’s better to wait or jump into the market.”

Consider the unique window that exists right now:

These are all opportunities that will go away if rates fall and demand surges. That’s why NAR says:

“Buyers who are holding out for lower mortgage rates may be missing a key opening in the market.”

Rates aren’t expected to hit 6% this year. But when they do, you’ll have to deal with more competition as other buyers jump back in. If you want less pressure and more negotiating power, that opportunity is already here – and it might not last for long. It all depends on what happens in the economy next.

Let’s talk about what’s happening in our area and whether it makes sense to make your move now, before everyone else does.

Are you wondering if you’re on track to retire someday?

According to Intuit, 69% of people say today’s financial environment makes it tough to plan for the future, and 68% aren’t sure they’ll ever be able to retire. That’s why many people are exploring new ways to build stability and long-term income.

And that’s where real estate comes in.

If you’re able to make the numbers work, buying a second home can be a powerful tool for your future retirement. It could help you:

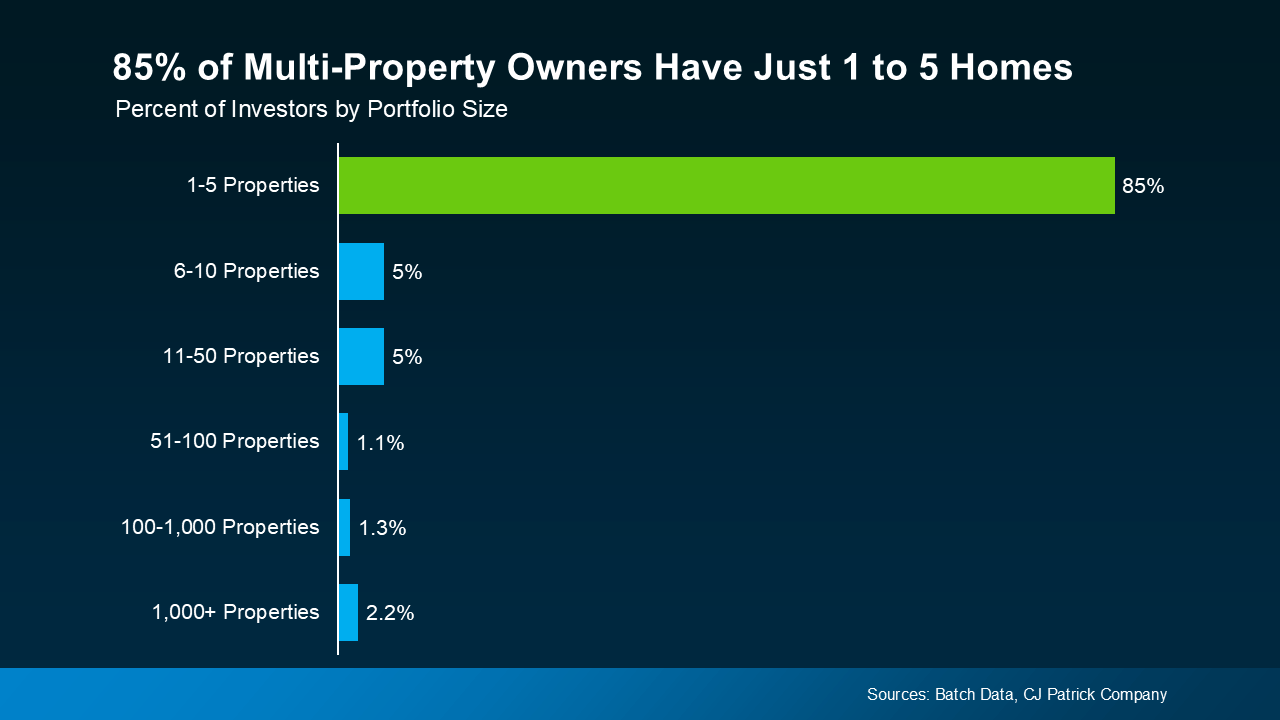

And if you’re thinking: wait, owning multiple homes is only for big investors – data shows that’s not necessarily true. Many homeowners who buy an additional property aren’t the big investors you hear so much about. They’re people like your neighbors.

In fact, data from BatchData and CJ Patrick Company shows 85% of people who own more than one property have just 1 to 5 homes (see graph below):

That means most who own multiple homes are people (not large investors) who’ve bought an extra home to rent out or hold onto for later.

That means most who own multiple homes are people (not large investors) who’ve bought an extra home to rent out or hold onto for later.

And right now, the door may be opening for buyers like you. According to Danielle Hale, Chief Economist at Realtor.com:

“. . . the balance of power in the housing market keeps shifting in favor of homebuyers. . . A confluence of factors—including more homes for sale, rising price cuts, and slower-moving inventory—is giving buyers more leverage than they’ve had in years . . .”

If you live in an area where home prices are expected to rise, buying another property now and selling it later could help fund your future. Or you could rent it out and earn income now.

If this idea sounds interesting, the most important first step is to connect with a few key people who can guide you through the process:

Surrounding yourself with the right pros can help you make confident decisions from day one.

Let’s talk about what’s possible and explore whether owning a second home could bring you more security and peace of mind for the road ahead.

If a second home could help you retire earlier or with more freedom, would you want to take a closer look?

Buying a home is exciting… until you start thinking about the down payment. That’s when the worry can set in.

“I’ll never save enough.”

“I need a small fortune just to get started.”

“I guess I’ll just rent forever.”

Sound familiar? You’re not alone. And you’re definitely not out of luck.

Here’s the thing: a lot of what you’ve heard about down payments just isn’t true. And once you know the facts, you might realize you’re a lot closer to owning a home than you think.

Let’s break it all down and bust some big down payment myths while we’re at it.

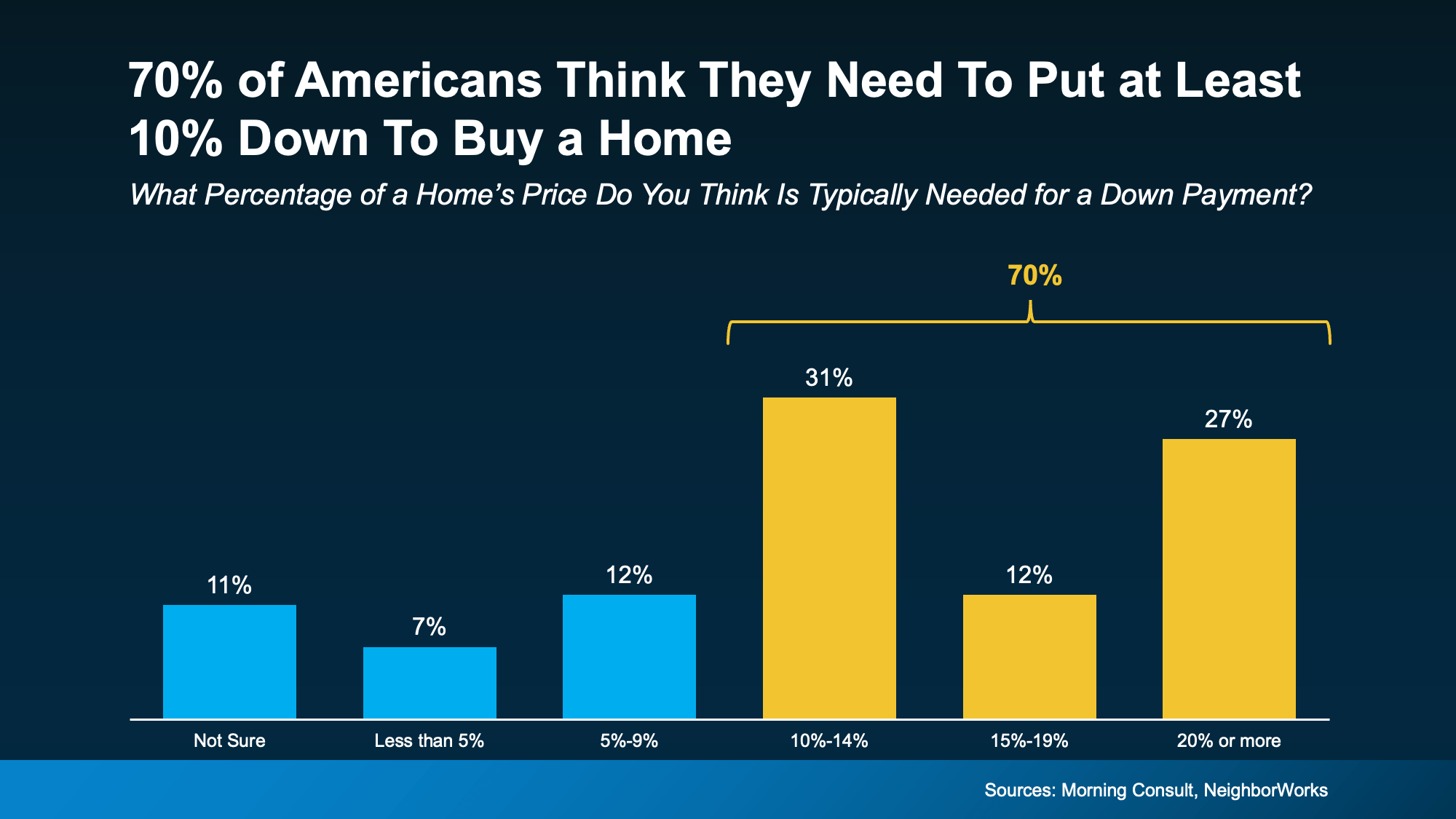

This one stops a lot of people in their tracks. A recent poll from Morning Consult and NeighborWorks shows 70% of Americans think they need to put at least 10% down to buy a home. And 11% aren’t sure what’s required at all (see graph below):

The truth? According to the National Association of Realtors (NAR), the typical down payment for first-time buyers has been between 6% and 9% since 2018. But there’s more to the story. If you qualify for an FHA loan, you may only need to put 3.5% down. And VA loans typically don’t require a down payment at all. So, there are options out there that can really make a difference for some buyers.

The truth? According to the National Association of Realtors (NAR), the typical down payment for first-time buyers has been between 6% and 9% since 2018. But there’s more to the story. If you qualify for an FHA loan, you may only need to put 3.5% down. And VA loans typically don’t require a down payment at all. So, there are options out there that can really make a difference for some buyers.

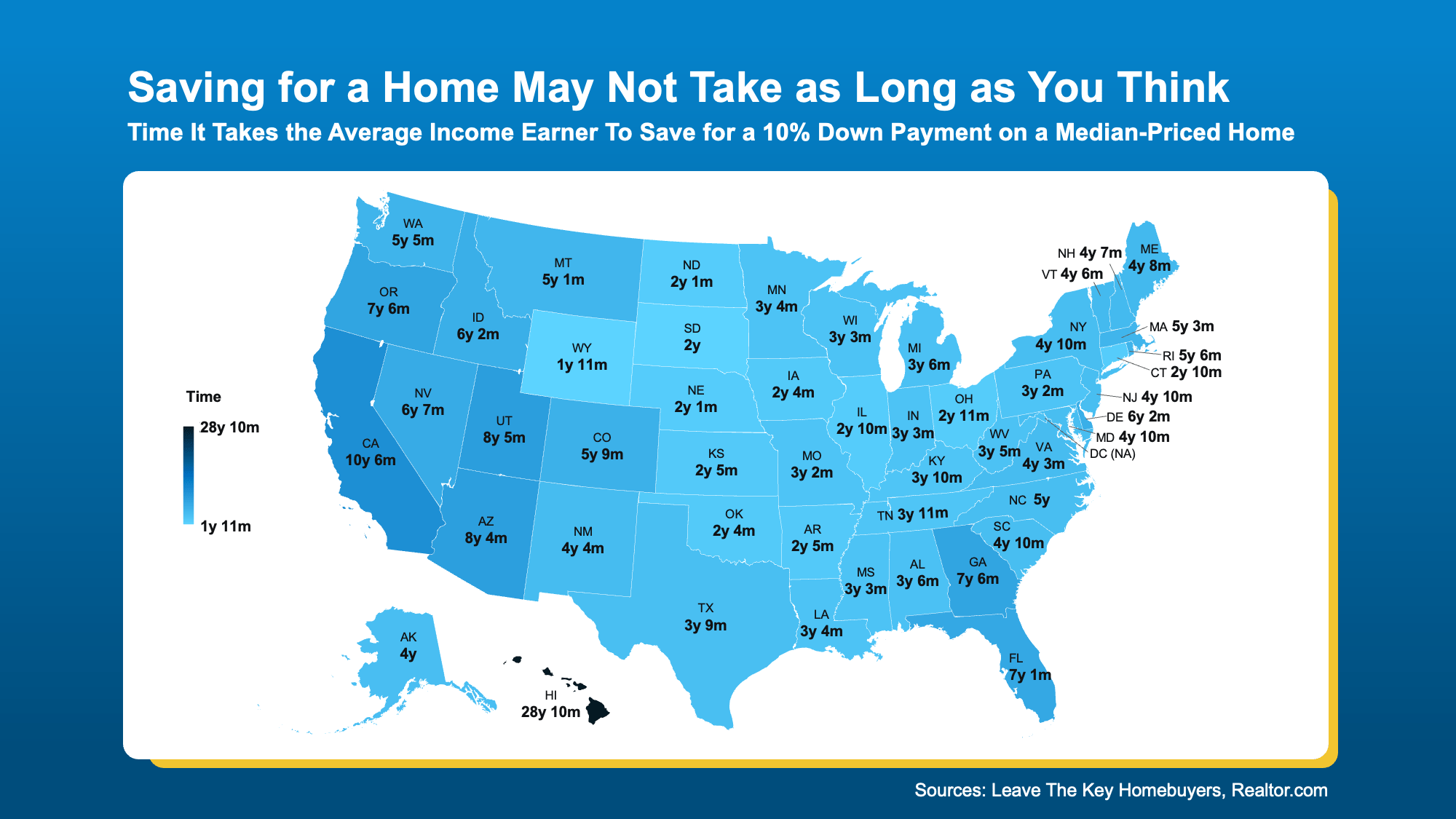

Sure, saving can take time. But it may not have to be as long as you think. In many states, reaching your goal can happen faster than you might expect, especially when you know your budget and have a clear savings plan.

According to a new study, the amount of time varies depending on where you live. The map below shows, on average, how many years it takes to save up for a 10% down payment based on typical home values and income levels in each state (see map below):

But remember, in most cases you won’t even need a down payment as large as 10%. Plus, no matter how much money you end up putting down, it won’t all have to come out of your pocket. Here’s why.

But remember, in most cases you won’t even need a down payment as large as 10%. Plus, no matter how much money you end up putting down, it won’t all have to come out of your pocket. Here’s why.

This is one of the biggest myths of all. The reality is, there are thousands of down payment assistance programs out there, and the same poll from Morning Consult and NeighborWorks shows 39% of people don’t even know about them. That means a lot of potential homebuyers could already be closer to homeownership – they just don’t realize it.

These assistance programs are designed to help people like you who are ready to own a home but just need a little support getting started. As Miki Adams, President at CBC Mortgage Agency, explains:

“With high interest rates and soaring home prices, down payment assistance is more essential than ever.”

If you’ve been putting off buying a home because the down payment feels like too much to tackle, let’s talk. You may not need as much as you think, and there are plenty of resources out there, so you don’t have to do it alone. You just need an expert to point you in the right direction.

If a down payment wasn’t holding you back, would you be ready to start your home search?